I  remember very clearly when we were purchasing our new home. There was some discussion about some Bubble Bursting in the Housing market. I didn’t understand what that meant, and doubted that it would ever really affect me personally.

remember very clearly when we were purchasing our new home. There was some discussion about some Bubble Bursting in the Housing market. I didn’t understand what that meant, and doubted that it would ever really affect me personally.

My oh My, how I was wrong…

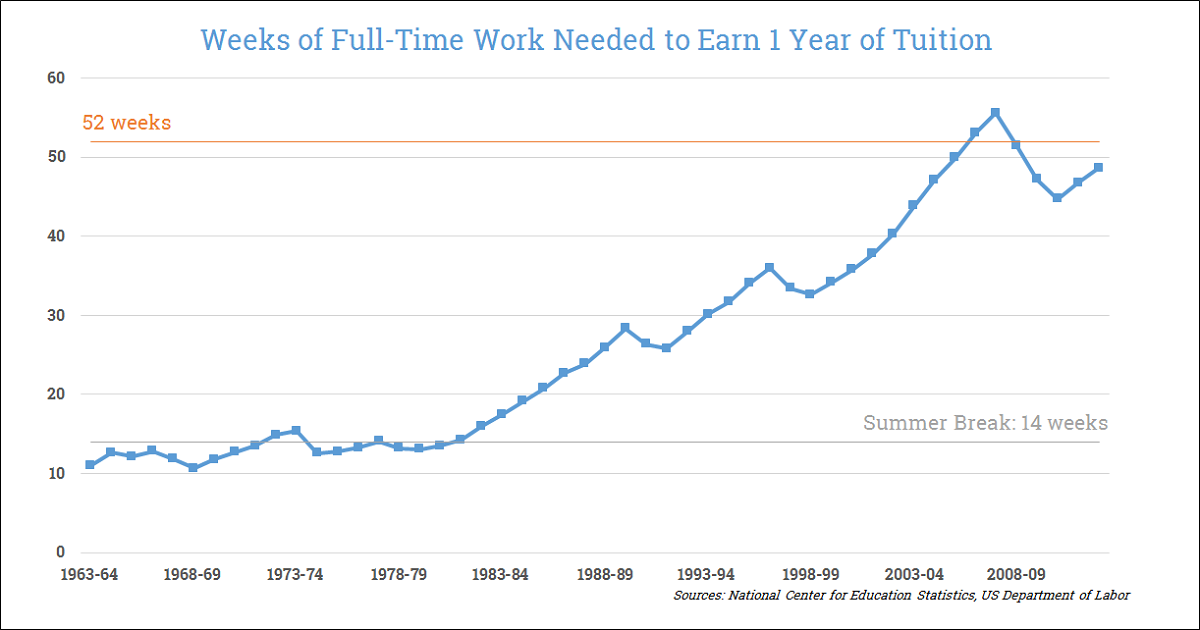

There has been discussion of another bubble for several years – the college loan bubble. As the price of attending college have soared, parents and students are taking out more and more loans in order to pay the bill. These loans are only available as long as investors and banks are willing to make the investment.

Recently a second major bank, JPMorgan has announced that they will be pulling out of the student loan market (US Bancorp stopped making student loans last year.). While there will still be financial aid available through the US Government, these changes will have an affect on the availability and affordability of college.

While you might not be able to avoid the bubble burst, you can think wisely about funding your college education.

1. Make sure you know (about education) before you go.

Once you hold that high school diploma, don’t automatically assume that you should go to college. There is an usual phobia that students (and parents) have that if you don’t go now, you will never go. It simply is not true.

Take the time to research on your own (or with a trained professional) concerning what you want to do for a job. Research the Outlook for the profession that you desire at the Bureau of Labor Statistics and Career Infonet. After narrowing down what you want to do, find an educational institution that can provide the knowledge and skills you need to get a job.

The goal of college is not a degree, the goal of college is to prepare you for the workplace. If you don’t need a four-year degree, then go to a trade or technical school.

College is still a good investment when you view the increased future earnings of college graduates, but make sure you finish your program. College debt with no job following graduation is hard. College debt with no degree is even harder.

2. Plan Ahead.

Planning ahead for the expenses of college is crucial in today’s world. Talk to a financial counselor, and start taking steps now to save money towards your education. Take advantage of AP high school classes, Clep tests, and PSEO programs that allow you start college for free while in high school. Programs are available in many states. As the market of higher educations makes changes, more and more options will become available.

3. Use debt sparringly.![blackfriday-consumerism-materialism-1251010-h[1]](http://www.earesources.org/wp-content/uploads/2013/09/blackfriday-consumerism-materialism-1251010-h1-300x225.jpg)

Get a job to pay for living expenses. Set a budget based on your future income (although you might not get a job right away), and don’t go over it. Refuse to use debt for the non-essentials like a new computer or smart phone, studying abroad (unless required by your degree), or late-night pizza orders.

4. Be wary of starting a university, if your attendance requires private funding.

If you are dependent on private funding and the bubble does burst, you may have to drop college, or transfer to another university (which always comes with additional expenses through losing credits). Many changes are coming to the world of education, especially to schools with high price tags (which includes most Christian schools). Changes need to occur in the Christian realm of higher education.

Many students shackle themselves to monstrous debt which seems to stand in opposition to the Bible’s teaching on money and debt. There is a huge need to take the warning of Proverbs 22:7 which says,

“Just as the rich rule the poor, so the borrower is servant to the lender.”

Whether or not the bubble bursts, following this college advice is bound to pay off for your future.

Dr. G. David Boyd is the Founder and Managing Director of EA Resources, who after writing this blog entry just texted a thank you note to his father for helping him make it through college.

Dr. G. David Boyd is the Founder and Managing Director of EA Resources, who after writing this blog entry just texted a thank you note to his father for helping him make it through college.

I wanted to share an

I wanted to share an

I recently came across an

I recently came across an

![wedding-baker-lianne-761857-h[1]](http://www.earesources.org/wp-content/uploads/2013/10/wedding-baker-lianne-761857-h1.jpg)

![blackfriday-consumerism-materialism-1251010-h[1]](http://www.earesources.org/wp-content/uploads/2013/09/blackfriday-consumerism-materialism-1251010-h1.jpg)

![DontDoTheMath[1]](http://www.earesources.org/wp-content/uploads/2013/07/DontDoTheMath1-300x200.jpeg)